How to Choose Between RRSP and TFSA: A Quick and Easy Guide

Wednesday Jan 17th, 2024

How to Choose Between RRSP and TFSA: A Quick and Easy Guide

If you’re a Canadian who wants to save money for your future, you’ve probably heard of RRSP and TFSA. In this post, I’ll explain the differences between these two popular savings accounts and help you decide which one to use for your retirement goals.

What is RRSP?

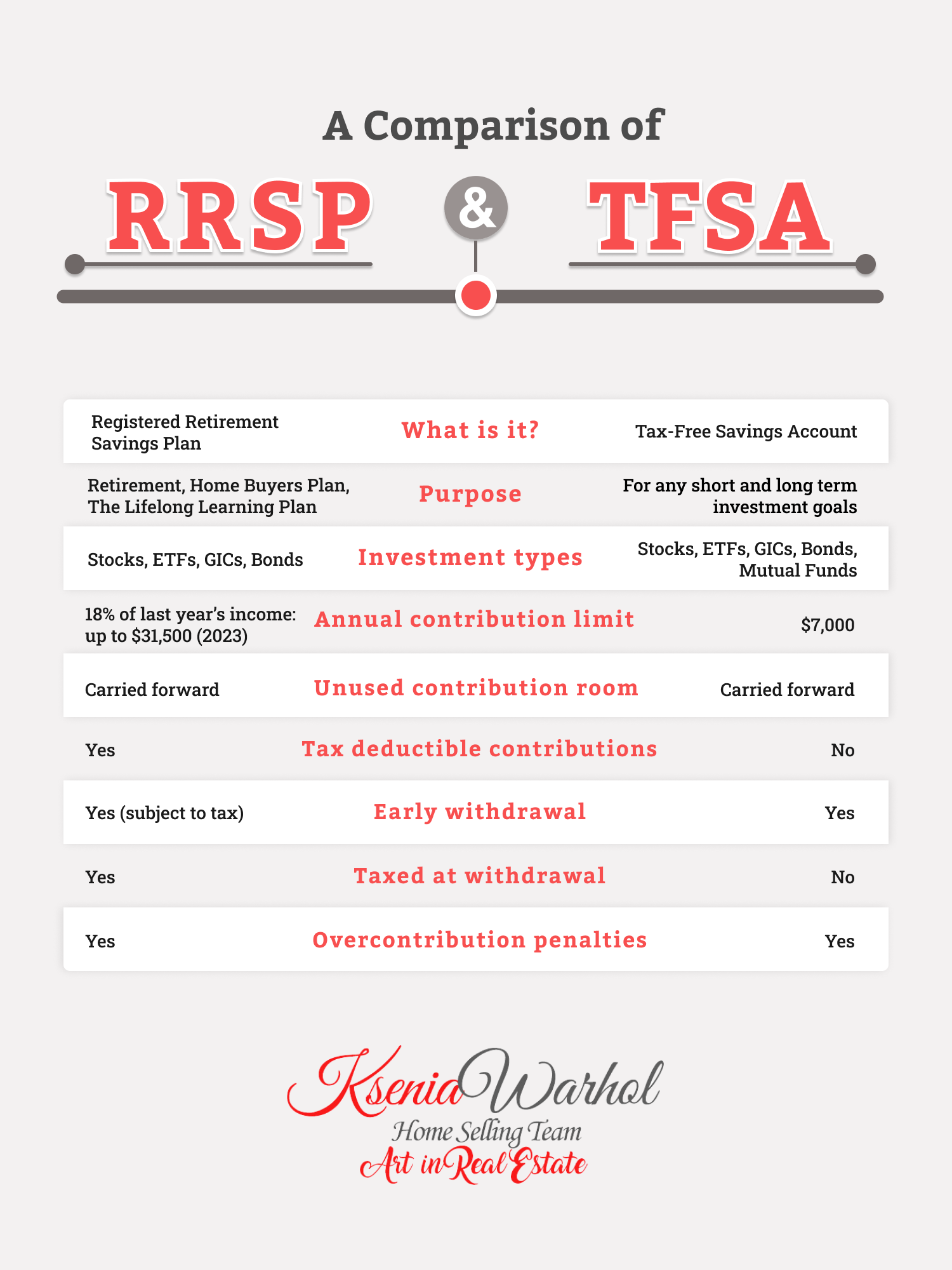

RRSP stands for Registered Retirement Savings Plan. It is a tax-advantaged account that lets you save and invest money for your retirement. You can contribute up to 18% of your last year’s income, up to a maximum of $31,500 in 2023. You can also carry forward any unused contribution room from previous years.

The main benefit of RRSP is that your contributions are tax-deductible, meaning you can lower your taxable income and pay less tax in the year you make the contribution. Your investments inside the RRSP grow tax-free, meaning you don’t pay any tax on the interest, dividends, or capital gains until you withdraw the money.

The main drawback of RRSP is that your withdrawals are taxed as regular income, meaning you may pay more tax in the year you take the money out. You also have to pay a penalty if you overcontribute to your RRSP, or if you withdraw the money before you retire, unless it’s for a specific purpose like buying your first home or going back to school.

What is TFSA?

TFSA stands for Tax-Free Savings Account. It is another tax-advantaged account that lets you save and invest money for any short or long term goal. You can contribute up to $7,000 in 2023, and any unused contribution room is also carried forward.

The main benefit of TFSA is that your withdrawals are tax-free, meaning you don’t pay any tax on the money you take out, regardless of your income level or the reason for withdrawal. Your investments inside the TFSA also grow tax-free, meaning you don’t pay any tax on the interest, dividends, or capital gains.

The main drawback of TFSA is that your contributions are not tax-deductible, meaning you can’t lower your taxable income or pay less tax in the year you make the contribution. You also have to pay a penalty if you overcontribute to your TFSA, or if you withdraw more than your contribution room in a given year.

How to choose between an RRSP and a TFSA?

There is no one-size-fits-all answer when it comes to choosing between an RRSP and a TFSA. It depends on your income, tax rate, time frame, risk tolerance and personal preference. However, here are some general guidelines to help you make an informed decision:

- If you expect your retirement income to be higher than it is now, you may want to use a TFSA rather than an RRSP, as you will pay less tax on the withdrawals than on your contributions.

- If you expect your retirement income to be lower than it is now, you may want to use an RRSP rather than a TFSA, as you will pay less tax on your contributions than you do withdrawing .

- If you have a short-term goal, such as saving for a vacation or a car, you may want to use a TFSA, as you can withdraw money tax-free or penalty-free each time.

- If you have a moderate income and want to save for both short and long term goals, you may want to use both RRSP and TFSA, because you can diversify your tax exposure and optimize your savings potential.

Post a comment