Your credit score is more than just a number; it represents your future home, the one you haven't bought yet.

By: Sofia Ryshun, based on Interview with Ksenia Warhol.

Think of your credit score as a reflection of your financial responsibility. It provides creditors and lenders with valuable insights into your financial behavior and creditworthiness. The higher your credit score is more likely you are to be approved for substantial loans, including a mortgage, at favorable interest rates and better conditions. On the other hand, a low credit score can make securing a mortgage difficult or, in some cases, even lead to outright rejection.

Based on my experience, individuals with credit scores of 700 or above usually receive the best mortgage rates and more favorable loan terms. However, I recommend having at least a credit score of 680 to get mortgage approval. Achieving and maintaining a good credit score is essential if you want to unlock the potential of homeownership.

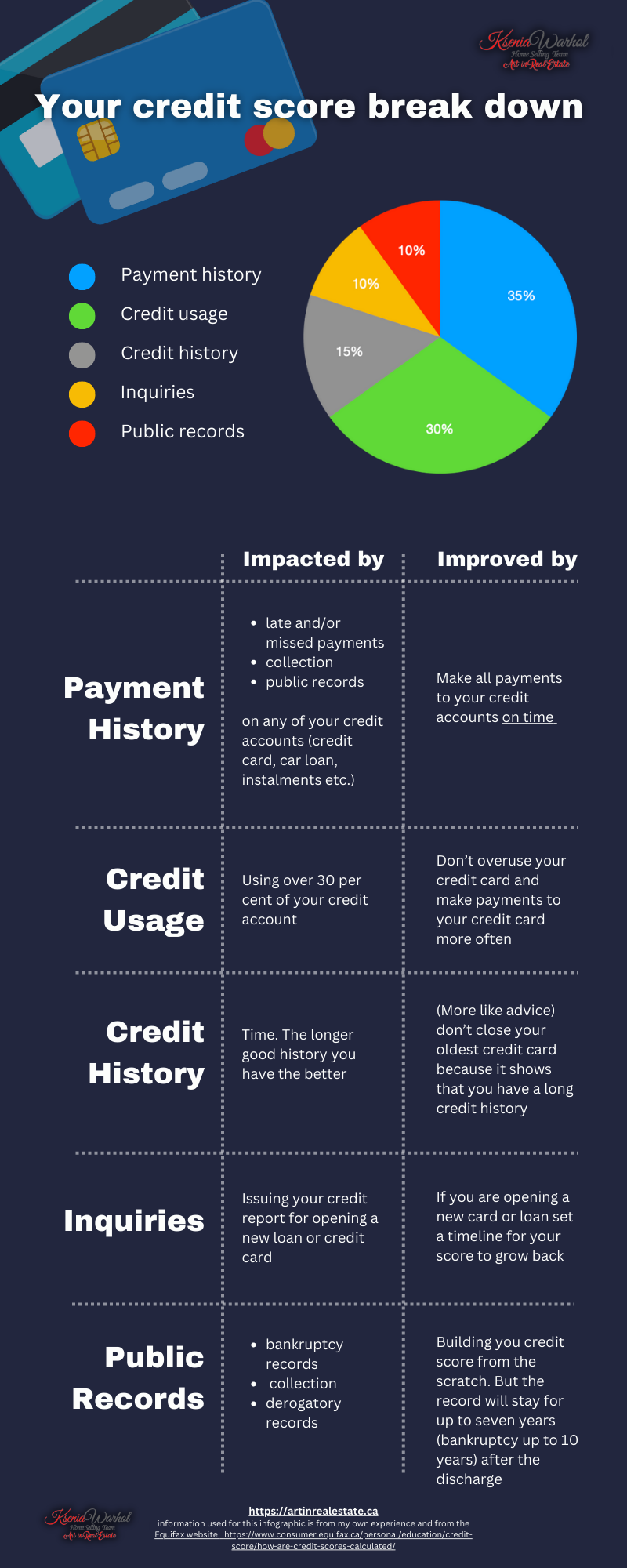

Factors Impacting Your Credit Score

- Payment History: Your payment history has a substantial impact on your credit score. Late or missed payments, as well as collections or public records related to any of your credit accounts (credit cards, car loans, installment plans, etc.), can lower your score. To improve your credit score, prioritize making all credit card payments on time.

- Credit Usage: The amount of credit you use compared to your credit limit is known as credit utilization. Using over 30 percent of your credit account can negatively impact your credit score. To improve this aspect, avoid overusing your credit cards and try to make more frequent payments.

- Credit History: The length of your credit history plays a role in determining your credit score. A longer and positive credit history demonstrates your experience in handling credit accounts, which is viewed positively by creditors. As a word of advice, avoid closing your oldest credit card, as it showcases a long credit history and contributes positively to your score.

Taking Charge of Your Credit Report

Sometimes, errors in your credit report can adversely affect your credit score due to inaccuracies in the information provided by creditors to the credit bureaus. In Canada, there are two credit bureaus: Equifax and TransUnion. To ensure the accuracy of your credit report, review it regularly and promptly address any mistakes. If you discover an error, write a letter to the creditor and/or credit bureau in question, requesting them to amend the mistake.

Post a comment